How to Invest for Doctors: A Self-Directed Guide for Low MER ETFs, Save Millions

Discover the benefits of low MER ETFs for long-term growth in our analysis at Scribeberry. Uncover the impact of fees on your investments and make savvy decisions today for a brighter financial future.

For many of us physicians, juggling the demands of a medical career with the complexities of finance can be daunting. Here at Scribeberry, our goal is to save you time and money. So every Tuesday, we will be sending informative content to help you achieve this goal from a neutral, bias free, sponsorship free, point of view.

This week, at Scribeberry: The AI Live Scribe company, we've deep dived into bringing you an analysis that explains easy passive investing through the world of low MER (Management Expense Ratio) ETFs. We'll break down the "whys" and the "hows" of embracing ETFs. Your future self will thank you for making this savvy decision today, as this may earn you over 2 million dollars or more in a 30 year career

1. What is a MER?

Let’s say you have 100k to invest. Most of us go to our bank and pick one of their nicely packaged funds (low vs medium vs high risk). When buying an investment through your bank, The Management Expense Ratio (MER) is a comprehensive metric that encapsulates the total cost associated with managing and operating an investment fund. These costs often encompass management fees, administrative fees, and several other operating expenses.

These MER costs are often thought of as minimal and are constantly overlooked

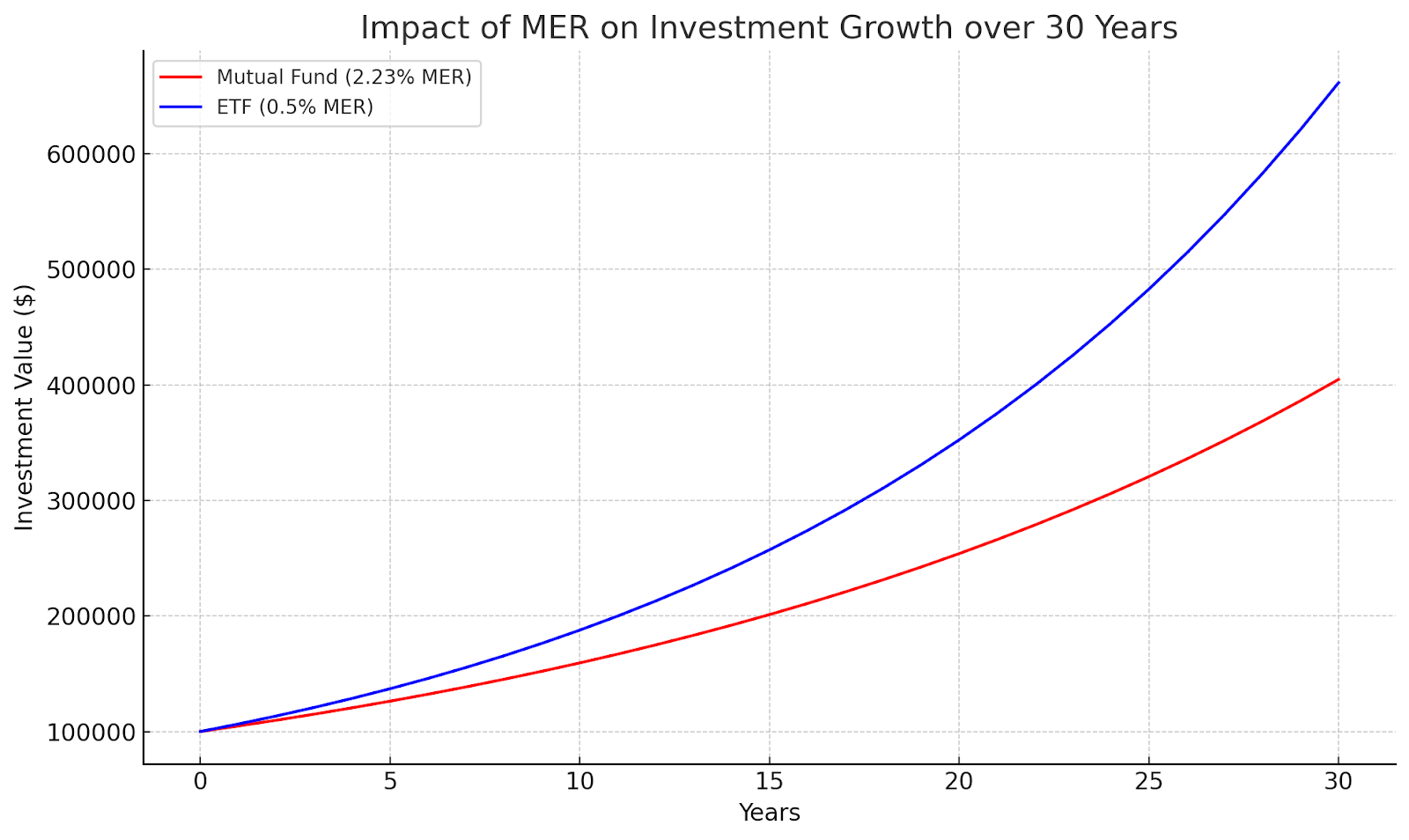

In the Canadian context, equity mutual funds typically come with an average MER hovering around 2.23%. These are usually bank packaged investment portfolios sold to you at face value as great investment options. In stark contrast, ETFs bought on your own often have an average MER below 0.5%, a fact that Scribeberry emphasizes as a significant differential for long term growth. Let’s run a scenario

2. Watch out for high MERs: a case study

To the uninitiated, the difference in MER between mutual funds and ETFs might seem minimal. However, the long-term ramifications of this difference are profound, thanks to the magic of compound interest.

Let's visit an example with a more detailed breakdown. Consider two investment avenues:

Investment A: A mutual fund from a leading bank championed by many but carrying a 2.23% MER

Investment B: A low-cost ETF, with a meagre 0.5% MER

For simplicity, both investments start with an identical gross return of 7% annually and an initial amount of $100,000. But what happens over three decades?

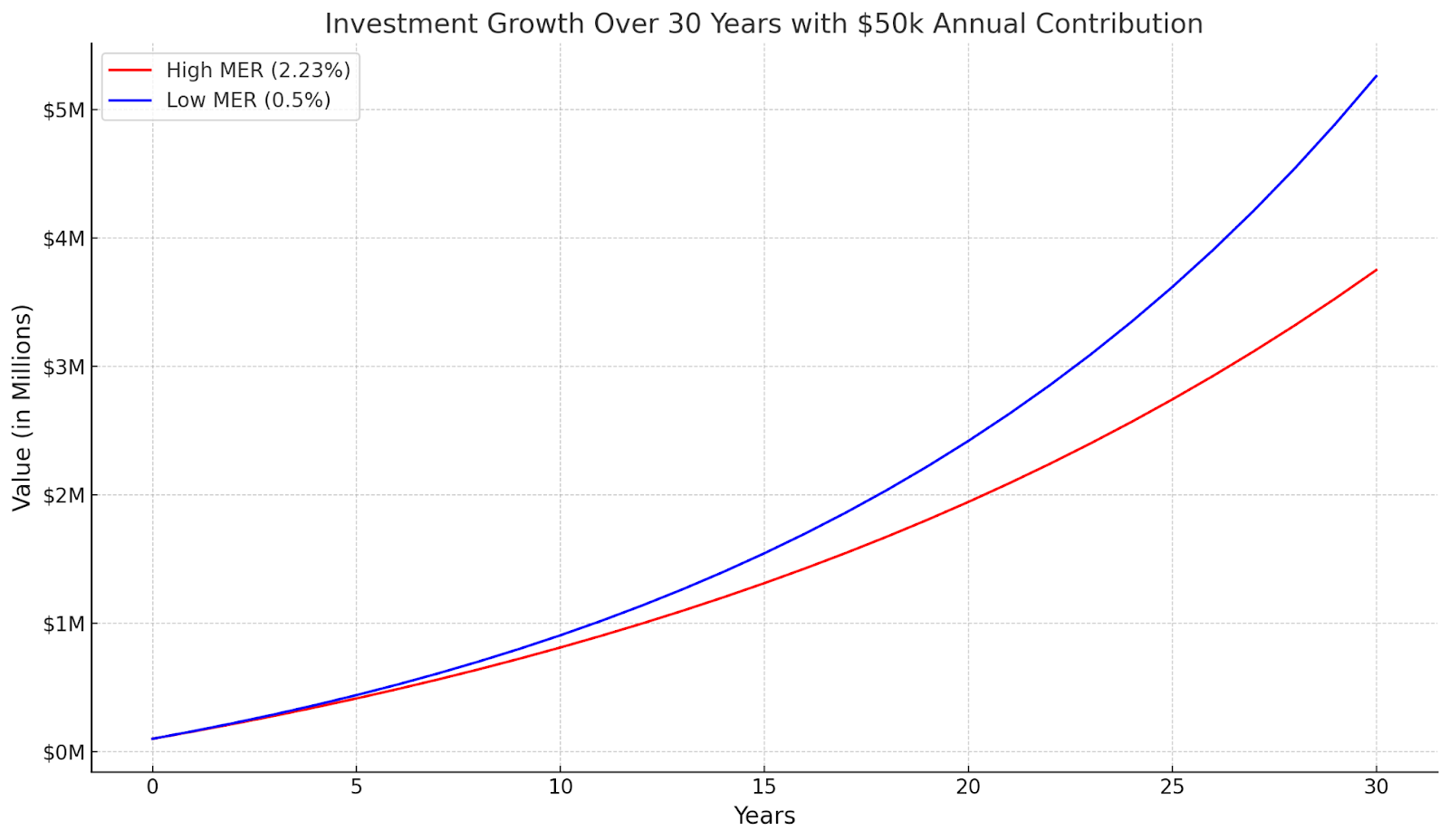

Now, Let's run the same scenario, but with a 100k initial investment and a 50k yearly additional investment over 30 years.

3. Say hello to ETFs

Beyond the evident cost-saving in MERs, low-cost ETFs bring a plethora of advantages to the table:

- Diversification: ETFs inherently track various indexes. This structure means that a singular ETF investment offers exposure to a broad market segment or sector. This diversification is vital for risk mitigation

- Liquidity: Unlike many other investment vehicles, ETFs are traded on stock exchanges, akin to individual stocks. This characteristic ensures that they can be bought or sold throughout the trading day, offering unparalleled flexibility and liquidity.

- Unbeatable Costs: The ScribeBerry analysis clearly showcases the immense savings potential when opting for low-cost ETFs purchased through exchanges over mutual funds. This cost advantage, especially in the Canadian context, can lead to significant gains over an extended period.

A minor 1-2% difference in fees may seem inconsequential in the short term. However, Scribeberry: The AI Live Scribe's analysis underscores the massive long-term implications of these seemingly trivial fees, thanks to compound interest.

4. What does this mean?

To match the growth of the ETF over 30 years, a financial advisor actively investing in the mutual fund with a 2.23% MER would need to consistently achieve an annual return of approximately 8.73% (gross), despite the higher MER. This is 1.73% higher than the 7% yearly return of the ETF.

Thus, the value a financial advisor would have to provide is essentially an ability to outperform the market (or our ETF example) by approximately 1.73% annually over the course of 30 years to justify the higher MER. This is practically unheard of.

5. Ok, how do I get started?

The steps to get started are pretty simple.

- Open a Brokerage Account and Move Funds

- Select a reputable Canadian online broker, such as Questrade, Wealthsimple Trade or Interactive Brokers to set up an account. Fund your account

- Research, Choose and buy a low-cost ETF (MER <0.5%)

Understand the basics of ETFs and identify those with low MERs that fit your financial goals. Pick one that encompasses the market (ie. VGRO). Invest yearly/monthly and ride the highs and lows of the market, rebalancing maybe once a year - focusing on long-term passive growth.

See below for a few of the ETFs with low MERs that we personally invest in. The charts show the daily prices year-to-date (YTD).

VGRO (TSX)

VUN (TSX)

VTI (NYSE)

We hope this has been helpful, please provide any feedback you may have. Additionally, if there is a topic you want to learn more about, let us know! Thanks for reading!

Come back every Tuesday for insights on how to save money and time. Our goal is to simplify and present objective advice across a range of topics to save you money and time. My goal is to help all of us optimize our experiences in life as doctors! Thank you for reading the Scribeberry AI Live Scribe blog.

About Us:

Scribeberry is an AI medical scribe tool for healthcare providers. If you are also interested in using Scribeberry, please try our app.

Mandatory Disclaimer: The information provided here is for general informational purposes only and is not intended to be financial advice. You are solely responsible for your own financial decisions and actions. Always conduct your own research and consider consulting a financial professional before making any investment. By using this information, you agree to take full responsibility for your decisions and any outcomes that may arise.